Eagers Automotive Limited

ASX:

APE

Eagers Automotive Ltd. engages in the management of automotive dealerships. Its activities include the sale of new and used vehicles, distribution and sale of parts, and accessories, repair and servicing of vehicles, provision of extended warranties, facilitation of finance and leasing in respect of motor vehicles, and the ownership of property and investments. It operates through the following segments: Car Retailing, Truck Retailing, Property, and Investment. The Car Retailing segment offers a range of automotive products and services, including new, used, maintenance and repair services, parts, extended service contracts, brokerage, and protection for vehicles. The Truck Retailing segment provides products and services, including new trucks, used, maintenance and repair services, parts, extended service contracts, protection, and other aftermarket products. The Property segment is the acquisition of commercial properties use as facility premises for its motor dealership operations. The Investment segment includes the investments in DealerMotive Limited, Automotive Holdings Group Limited, Smartgroup Corporation Limited, and Dealercell Holdings Pty Limited. The company was founded by Edward Eager and Frederick Eager in 1913 and is headquartered in Brisbane, Australia.

Stock Performance Profile:

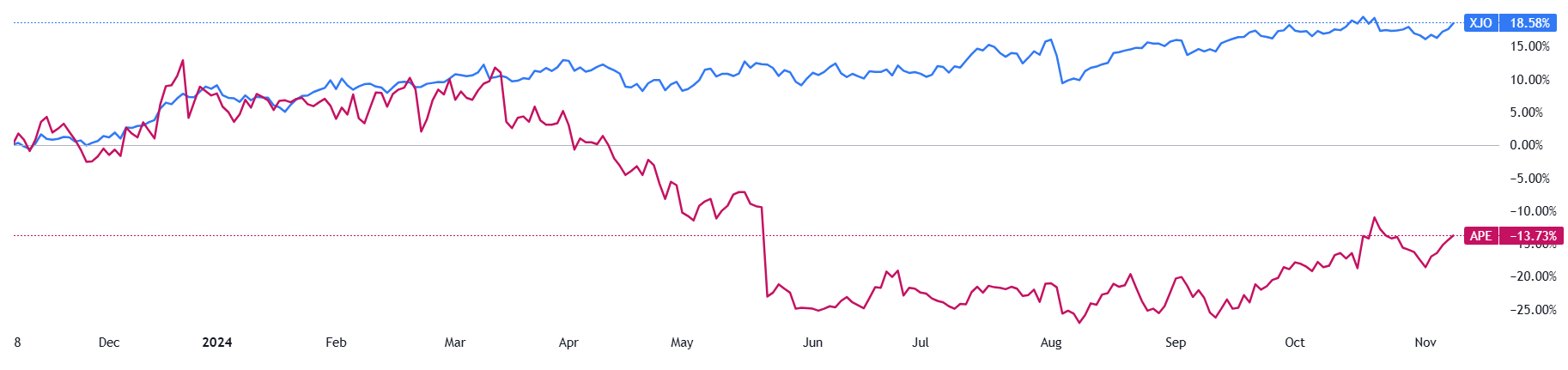

(Source: TradingView) One-Year Performance Profile of APE compared to ASX 200 (XJO).

From the Company Reports:

Eagers Automotive Limited (ASX: APE) has recently published its half-yearly financial results for the first half of FY24, concluding on 30 June 2024.

The company achieved record first-half revenues amounting to $5.46 billion, representing a significant 13% increase from $4.82 billion in the same period last year.

However, the company’s earnings experienced a decline, falling from $137 million in the previous corresponding period to $116 million.

This decrease can be attributed to the clearance of surplus inventory, which adversely affected the profit contributions from its Retail Joint Venture.

Despite this, the company’s financial standing remained strong at the end of the reporting period, with available liquidity reported at $444.7 million as of 30 June 2024.

Financials:

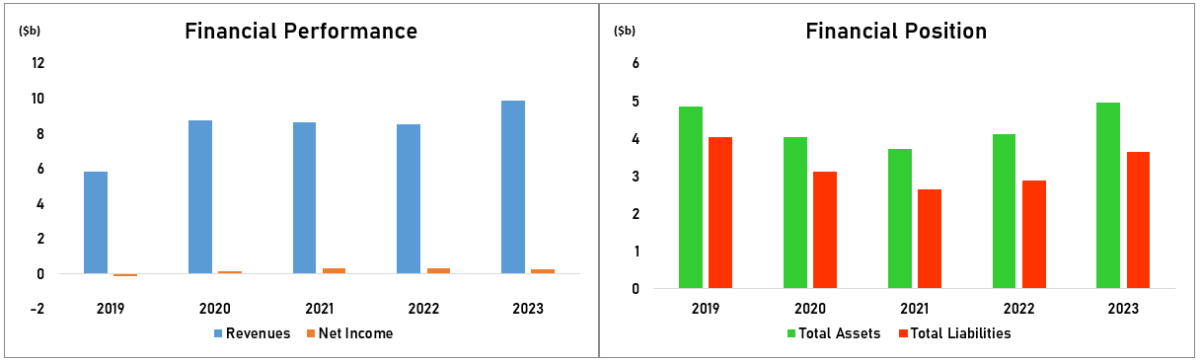

(Data Source: TradingView. Graphic Source: Pristine Gaze)

The company has faced a period of earnings stagnation in recent years, consistently hovering around the $300 million threshold. However, it is important to highlight that its long-term growth trajectory remains exceptional, having successfully reversed a loss of $142 million in 2019 and annual profits of under $100 million in the preceding years to achieve substantial earnings growth in subsequent years. During this same period, the company’s revenues have surged impressively, rising from $5.8 billion in 2019 to $9.85 billion in 2023, with recent data indicating continued record highs into 2024. Furthermore, the company’s financial health has markedly improved, as evidenced by an increase in its asset base from $4.86 billion in 2019 to $4.95 billion in 2023, alongside a significant reduction in liabilities from $4.04 billion to $3.64 billion. This has led to a notable enhancement in the book value for shareholders, reflected in the rise of book value per share from $3.16 in 2019 to a record $4.94 in 2023.

Dividend Profile:

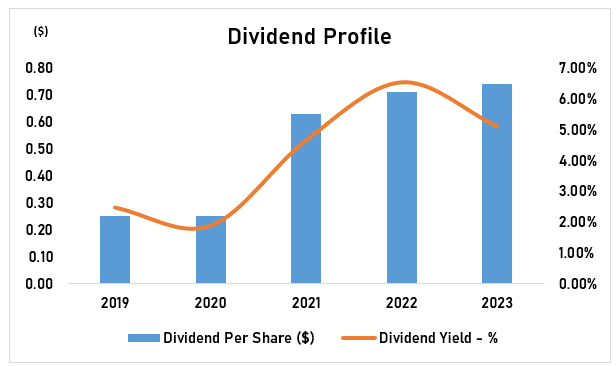

(Data Source: TradingView. Graphic Source: Pristine Gaze)

The graphic presented above underscores the company’s commitment to enhancing distribution growth for its shareholders, evidenced by a consistent and substantial rise in annual dividend payments from $0.25 per share in 2019 to $0.74 per share in 2023. This represents an impressive increase of nearly 300% over a five-year span. Consequently, the yield for shareholders has markedly improved, escalating from 2.47% in 2019 to 5.11% in 2023, and currently approaching its peak at 6.49%.

Investment Rationale:

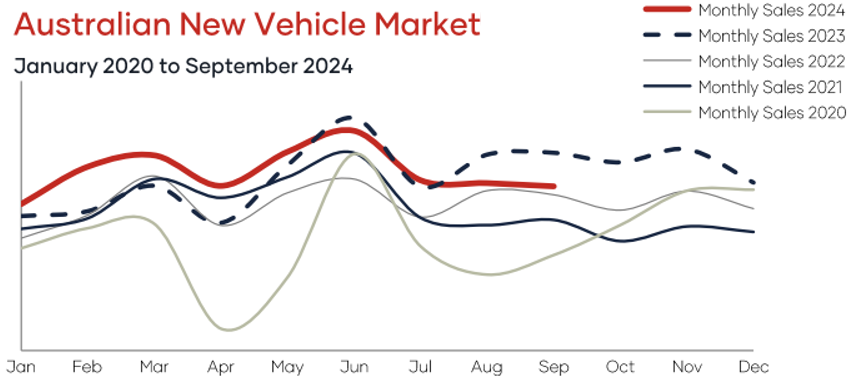

(Graphic Source: Company Reports)

Eagers continues to benefit from a robust market demand for new vehicles in Australia, with sales showing substantial improvement relative to previous years. This demand has notably surpassed historical levels, facilitating record delivery rates in seven of the past twelve months. The company’s inorganic growth strategies are particularly significant; as its recent Retail Joint Venture initiative has greatly enhanced its market footprint via retail partners. Additionally, ongoing acquisition efforts and the integration of prior acquisitions are anticipated to foster overall business growth and optimization. Coupled with a strong industry position and competitive customer offerings—including financing solutions and customer support—these elements are expected to drive sustained sales and operational growth for Eagers over an extensive period.

Outlook:

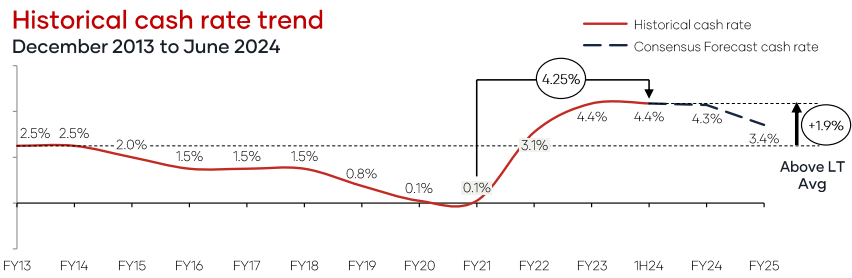

(Graphic Source: Company Reports)

The recent earnings performance of the company has been significantly hindered by substantial interest expenses. Although recent statements from the Governor of the Reserve Bank of Australia (RBA) suggest that immediate interest rate reductions are unlikely in the near term, it was noted that any indications of declining inflation or decreased market activity could prompt such cuts. These potential rate reductions are anticipated to yield considerable cost savings for the company in the long run, with each 25 basis point (bps) decrease is projected to save approximately $6 million. Additionally, the company’s emphasis on improved inventory management is expected to enhance profit margins, as a reduction of just one day in its operating cycle could result in cost savings of around $3 million.

Technicals:

(Graphic Source: TradingView) Eagers Automotive Limited (ASX: APE) Weekly Time-Frame (WTF) Chart.

The security exhibits a robust support level near $11, coinciding with its 14-Day Exponential Moving Average (EMA) and the nearest Fibonacci retracement level. Historically and recently, the stock has demonstrated resilience by rebounding from this price point on several occasions. The recent interaction of the security with its 50-Day EMA, following a crossover above the 14-Day EMA, suggests the possible initiation of a favorable upward trend. Additionally, the 14-Day Relative Strength Index (RSI) is on the rise, currently at 54.25, indicating a healthy level of market buying activity.

Analyst’s Take:

Eagers has faced unfavorable market sentiment recently, primarily due to sluggish earnings growth in 2023 and a slight decline in earnings during the first half of 2024. However, the company’s earnings are anticipated to rebound in the latter half of 2024 and continue to grow significantly in the following years. This positive outlook is largely attributed to the company’s remarkable and sustained sales growth, coupled with concurrent factors reducing costs and enhancing profit margins. Furthermore, Eagers also provides a compelling value proposition, as its valuation metrics have markedly improved compared to previous years and remain appealing on an independent basis, evidenced by a price-to-earnings (P/E) ratio of 11.44x, a price-to-sales (P/S) ratio of 0.28x, and a price-to-book (P/B) ratio of 2.33x. The company’s balance sheet is robust, and its strong liquidity position is expected to alleviate potential monetary risks. Collectively, these elements, along with an attractive dividend yield and consistent growth in distributions, offer promising opportunities for both capital appreciation and substantial income generation for investors.

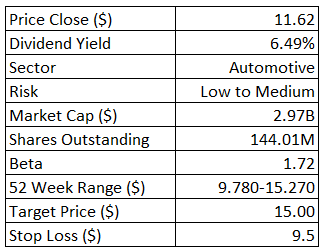

As per Pristine Gaze, you may consider a “Buy” on “Eagers Automotive Limited” at the closing price of “$11.62” (As of 8 November 2024).

*All currency figures are in Australian Dollars unless stated otherwise.

*All data sourced from Company Reports and TradingView.

Disclaimer

The reports provided by Pristine Gaze are designed to deliver comprehensive stock and sector analysis, market insights, and investment recommendations, drawing upon our research and expertise. However, it is important to note that these reports are intended for informational purposes only and do not constitute personalised financial advice. They do not consider your individual investment objectives, financial situation, or specific needs.

Before making any investment decisions based on the insights and recommendations included in these reports, we strongly advise consulting with a qualified financial advisor who can provide tailored advice that aligns with your personal circumstances.

Pristine Gaze, including its directors, employees, associates, and affiliates, assumes no liability for any loss or damage incurred as a result of relying on the information or recommendations provided in these reports. This encompasses, but is not limited to, direct, indirect, incidental, or consequential losses.

While we endeavour to ensure the accuracy and timeliness of the information presented in our reports, we cannot guarantee its completeness or accuracy, and the content may change without prior notice. The inclusion of any stock or sector within these reports does not serve as an endorsement or recommendation, and such mentions may be altered or removed at any time.

These reports may reference external data or links to third-party resources, for which Pristine Gaze takes no responsibility. The use of such information or resources is at your own risk.

All content within the Pristine Gaze reports, including but not limited to text, graphics, and analysis, is the intellectual property of Pristine Gaze and is protected under applicable copyright and trademark laws. Unauthorised use or distribution of this content without prior consent is prohibited.

By accessing or utilising Pristine Gaze’s reports, you acknowledge and agree to the terms outlined in this disclaimer. For further details, please refer to our full Terms and Conditions and Privacy Policy.